Call Bob Moulton Today: (917) 627-0200 • Email: RobertMMoulton@gmail.com

A Look Into The Markets

As summer nears the end, home loan rates took a pause on their recent uptick. Let's discuss what happened and look at the important week ahead.

"Stop! In the name of love, before you break my heart"... Stop! In the Name of Love - The Supremes

Mortgage Rates At 21 Year Highs

The big news in mortgage and housing has been the recent and rapid rise in home loan rates. Early in the week, they reached 7.50%, to levels last seen in 2002.

What has been causing rates to climb in recent weeks?

- The big increase started when the Treasury Department requested an additional $275B in late July to fund the government between August and October.

- The increase in spending prompted Fitch Ratings to downgrade U.S. debt, citing "fiscal deterioration".

- Fears of a recession have evaporated.

- The Fed is close to finishing rate hikes, yet inflation remains high.

- Oil has climbed which is elevating inflation fears.

- Japan and China selling their holdings of Treasuries.

The good news? On Wednesday, interest rates declined sharply, helping rates improve from these multi-year highs.

So, what created the pause in the rise in rates this week?

- Bad news is good news. Global economies are slowing rapidly leading to a decline in global bond yields.

- A sharp decline in oil, back under $80 a barrel, lowering inflation fears.

- Anticipation of next week's action-packed economic report calendar. Markets are not placing any large bets.

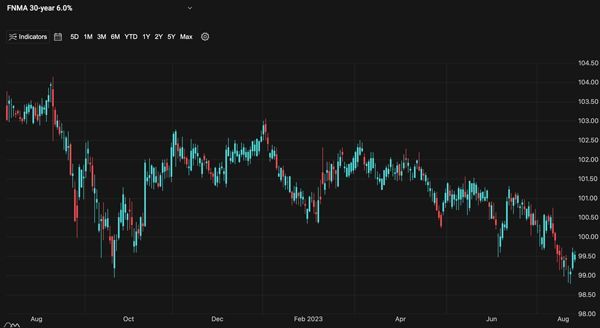

- Mortgage Bonds hit exactly at the October price lows and bounced higher. Look at the chart below.

Oil

Oil prices moved lower on lower demand fears and a stronger U.S. Dollar. This is an important story because if Oil moves above $84, there is a real threat of $90+ oil and quickly. Seeing Oil retrace back to $78 is good news for inflation and interest rates.

Fed Rate Hike Chances

Right now, the chance of a Fed rate hike in September is just 15%. But, the chance of a Fed rate hike in November is 40%. Whether the Fed hikes now or in November, the markets are looking forward and sensing the Fed is finished hiking and moving to a position of "how long" they can keep rates high until inflation falls back down to 2%. This uncertain story will remain with us for the foreseeable future but it is worth a reminder that mortgage rates are not controlled by Fed rate hikes as evidenced by the lists above.

Housing, A Tale Of Two Markets

The spike in home loan rates has put a damper on the housing market, but it is affecting existing and new home sales differently. The spike in rates clearly makes it a challenge for someone with a far lower mortgage rate to list their home for sale. This has created an inventory problem as well as keeping prices high.

But in a housing bright spot, builders are having their way as demand for housing remains robust, material costs have normalized, and builders can get creative with programs to get homebuyers into properties.

Bottom line: Home loan rates paused their rise and next week we may find out if the retreat in rates is sustainable. Housing remains in a long-term bull market and upon any meaningful decline in rates, we should expect housing to also step off the pause button, with activity quickly resuming.

Looking ahead

Next week might be the biggest economic news week of the year. With just a few weeks before the next Fed Meeting, we will see reports on inflation, the labor market and economic growth. If the reports show weakness, it may very well confirm the Fed is no longer hiking rates, the opposite is true.

Mortgage Market Guide Candlestick Chart

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 6.0% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

On the right side of the chart, you can clearly see how prices have rebounded higher from the exact price lows/rate peaks of October. If prices remain above these bottoms, we will see some stabilization in rates. But if prices fall beneath this floor, we will see home loan rates rise to the highest level in this century. Fingers crossed.

Chart: Fannie Mae 30-Year 6.0% Coupon (Friday, August 25, 2023)

Economic Calendar for the Week of August 28 - September 1

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is without errors.

As your mortgage professional, I am sending you the MMG WEEKLY because I am committed to keeping you updated on the economic events that impact interest rates and how they may affect you.

Mortgage Market Guide, LLC is the copyright owner or licensee of the content and/or information in this email, unless otherwise indicated. Mortgage Market Guide, LLC does not grant to you a license to any content, features or materials in this email. You may not distribute, download, or save a copy of any of the content or screens except as otherwise provided in our Terms and Conditions of Membership, for any purpose.

Registered Mortgage Broker-NYS Department of Financial Services

All mortgage loans arranged with third party providers.

NYS, CT, NJ, FL Department of Financial Services