Call Bob Moulton Today: (917) 627-0200 • Email: RobertMMoulton@gmail.com

Mortgage rates spiked to the highest level since early July, despite the Federal Reserve cutting rates again. Let's discuss what happened and what to look for in the weeks ahead

"We walk blind and we try to see, falling behind in what could be, Bring me a Higher Love" by Steve Winwood.

The Fed Meeting

As expected, the Federal Reserve cut interest rates by 0.25%. Since September, the Fed has lowered the Fed Funds rate by 1.00% down to 4.25%. This rate cut affects short-term rates like auto loans, credit cards, and home equity lines of credit. What it doesn't help is mortgage rates - in fact, since the rate cuts began in September, they have only worsened.

Wednesday was no different, as long-term rates spiked sharply higher. The 10-year Note, which ebbs and flows with mortgage rates, spiked to 4.55%. On September 16th, the 10-year Note stood at 3.66%, just two days before the Fed started cutting rates.

Inflation Remains an Issue

If there were one word to describe why rates spiked, causing stocks and crypto to suffer, that word would be inflation. Fed Chair Powell, in his press conference, said that the lack of progress in further lowering inflation has been disappointing. The bond market seized on this lack of confidence to rein in inflation by pushing rates higher. If inflation remains high, long-term rates will also remain higher.

Summary of Economic Projections

In addition to lowering rates, the Fed issued its Summary of Economic Projections. This is something it revises every three months. Here is what the Fed now sees happening in the economy.

In 2025, it sees economic growth slightly stronger, unemployment lower, and inflation higher than previously expected. For these reasons, the Fed now anticipates just two rate cuts next year instead of the four previously forecasted back in September.

The forecast may be optimistic regarding unemployment. The Fed predicts unemployment peaking at 4.3%, which is slightly above the current rate of 4.2%. If the Fed is incorrect with its forecast and unemployment rises, it will likely cut rates more than expected because it states, "further weakening in the labor market would be unwelcome."

Press Conference

After each Fed meeting, the Fed Chair holds a press conference where he takes questions and provides answers. At the press conference on Wednesday, it was clear that Mr. Powell sees inflation returning to their 2% target more slowly than they would like and what was previously forecasted.

Again, this uncertain outlook on inflation was unnerving to the financial markets.

Not Unanimous

Not everyone wished to cut rates. Cleveland Fed President Beth Hammack voted against the 0.25% rate cut and preferred not to cut. This shows that Fed members are likely to be very careful with cutting rates going forward and will respond to the data.

Bottom Line: Rates have continued to creep higher ever since the Fed started cutting rates, as fears of inflation reaccelerating emerge. Going forward, the incoming economic data will be very important to follow, and any weakness in inflation or unemployment will help rates—the opposite is also true.

Looking Ahead

Next week, the economic calendar is a bit thin, with only a few moderate-impact releases. However, we will have several Fed officials speaking and sharing their thoughts on the economy and interest rates.

Mortgage Market Guide Candlestick Chart Mortgage bond prices determine home loan rates. The chart below provides a one-year view of the Fannie Mae 30-year 6% coupon, where currently closed loans are being packaged.

As prices move higher, rates decline, and vice versa. If you look at the right side of the chart, you can see how prices have declined to the lowest levels since July 4th.

Chart: Fannie Mae 30-Year 6.0% Coupon (Wednesday, December 20, 2024)

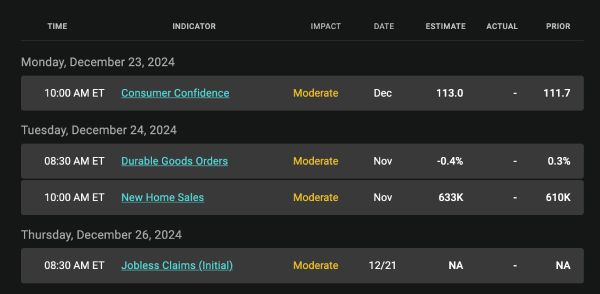

Economic Calendar for the Week of December 23 - 27

Registered Mortgage Broker-NYS Department of Financial Services

All mortgage loans arranged with third party providers.

NYS, CT, NJ, FL Department of Financial Services